Q2 Performance. Is Size a Winning Strategy? Where Are They Now?

Q2 Peformance

Q2 was a productive quarter for most law firms, according to Thomson Reuters Law Firm Financial Index which tracks and analyzes billing and financial data for 171 U.S.-based law firms, including 51 Am Law 100 firms, 55 Am Law Second Hundred firms, and 65 Midsize firms (Law Firm Financial Index Q2 2024 Executive Report “LFFI Report”, 8/5/24). Most practice areas experienced demand growth relative to Q2 2023.

Demand growth was not consistent among law firm segments, however. The AmLaw 100 saw most of their growth in transactional practices; in fact, the AmLaw 1-50 saw a 4% dip in litigation demand. Litigation and other counter-cyclical practices fueled demand growth for Midsize firms. And the Second Hundred "found a Goldilocks zone, benefiting from significant growth in both areas [litigation and transactional]."

The demand growth was not due to rate discounts; in fact, firms continued to push through rate increases. Q2 2024 saw worked rate grow 6.6% over Q2 2023, a new record for the Law Firm Financial Index, following 6.4% rate growth in Q1 2024, a record at the time. Per usual, the AmLaw 100 were the most successful in raising rates, registering over 10% worked rate growth in Q2 2024 over Q2 2023.

Bill Josten, content manager for Thomson Reuters, told the American Lawyer that firms have been "very aggressive" with rates since 2022. And firms that were initially conservative are now jumping on board, after seeing the success of their peers in raising rates (Law Firms Look 'Stronger Than Ever,' Even Compared with Transactional Boom, Andrew Maloney, 8/5/24, American Lawyer).

Is Size a Winning Strategy?

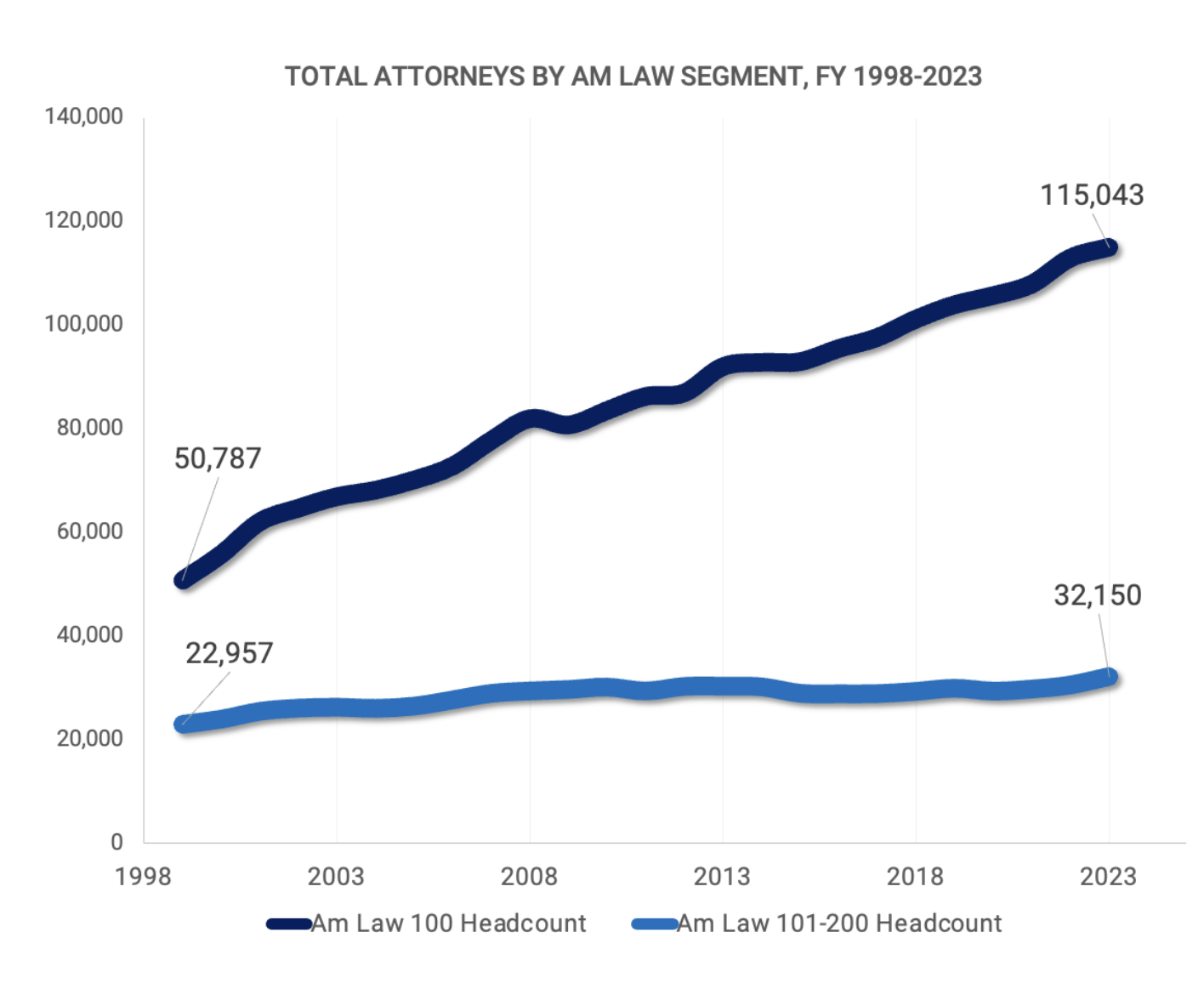

Over the last 25 years, the AmLaw 100 has increased headcount at a staggering rate relative to the Second Hundred (Law.com Pro Executive Briefing "Briefing", Gina Passarella & Patrick Fuller, 6/24/24, American Lawyer). The average AmLaw 100 firm's headcount increased 147% since 1999, while the Second Hundred grew at only 40%, as illustrated in this graph from the Briefing.

Over this period, the AmLaw 100 also grew Revenue per Lawyer (RPL), Profit per Lawyer (PPL), and Profit per Equity Partner (PEP) at a faster rate than the Second Hundred (Briefing).

Relative growth in these key financial measures could lead to the conclusion that headcount/revenue growth for growth's sake is a winning strategy. However, the Briefing also points out that the 20 firms with the highest revenue growth over the last 5 years ranked in the middle of the AmLaw 200 for RPL, PPL, and PEP over that same time period, cautioning that growth can lead to overcapacity, "resulting in more production but not necessarily better production." Moreover, a key component of the AmLaw 100's relative success has been their ability to increase rates, especially in recent years when many firms outside of the AmLaw 100 have struggled to keep rate growth above inflation (Briefing).

Where Are They Now?

The Briefing also analyzed where firms in the 1999 AmLaw 200 Survey rank in 2024. Interestingly, roughly 1/3 of those firms are no longer in existence (12% dissolved and 22% were acquired or were the secondary firm in a merger). And 63% are still active in the AmLaw 200 under their primary brand name (55%) or the name of a merged entity in which they were the primary firm (8%).